TAKEAWAYS

With the Chinese New Year festivities behind us, we are now approaching the personal tax filing season for the year of assessment (YA) 2025 for individual taxpayers in Singapore. Depending on the mode of filing, individual taxpayers are required to file their personal tax returns by April 15 or 18. Failing which, adverse consequences, such as fines and penalties, may be imposed by the Inland Revenue Authority of Singapore (IRAS). Now, in the course of complying with the personal tax filing requirements in Singapore, would you also be communicating financial information with your family members?

In the Asian context, the communication of financial information between family members is uncommon. Why? This may be due to various cultural, social and practical reasons. Firstly, sharing financial success may be viewed as boastful, which is contrary to the culture of humility. Secondly, discussing financial matters that are highly private and sensitive may be regarded as intrusive, which is socially inappropriate. Lastly, disclosing financial status may lead to excessive expectations of family support, which is the norm in collectivist society.

However, against the backdrop of personal tax filing in Singapore, should you communicate financial information with your family members?

In Singapore, the personal tax regime is often used as a tool for the promotion of certain social (and economic) goals. This is evident from the claiming of personal reliefs and rebates by individual taxpayers – the former has the effect of reducing income tax payable indirectly (through reducing income chargeable to tax), while the latter has the effect of reducing income tax payable directly (akin to a discount on tax bills). Examples of pro-family reliefs and rebates in the country include parent/handicapped parent relief, handicapped brother/sister relief, spouse/handicapped spouse relief, qualifying/handicapped child relief, working mother’s child relief, grandparent caregiver relief, and parenthood tax rebate.

The claiming of personal reliefs and rebates is not without conditions. More often than not, a certain level of financial information needs to be communicated with family members to prevent wrongful claims. For example, to claim parent relief, spouse relief and qualifying child relief, the subject of claim (that is, the parent/grandparent, parent/grandparent-in-law, spouse and child) must not derive annual income of more than $8,000 in the basis period effective from YA 2025 ($4,000 prior to YA 2025). For the avoidance of doubt, annual income includes taxable income, exempt income and foreign-sourced income (regardless of remittance), among others.

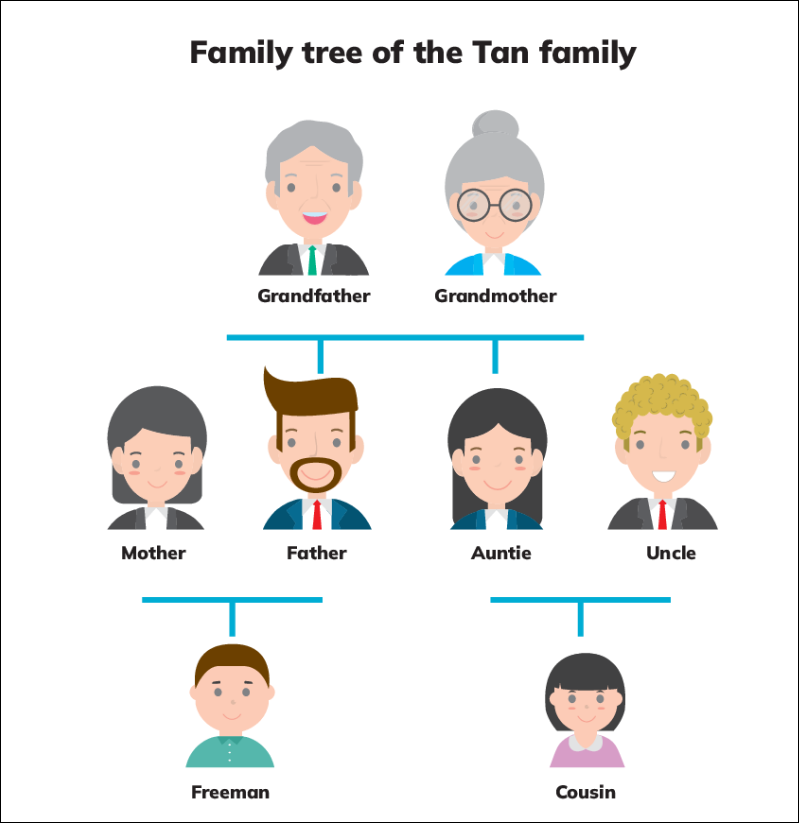

In addition to the prevention of wrongful claims, the communication of financial information between family members facilitates tax planning. This is due to the following features of the pro-family personal reliefs and rebates: (a) certain personal reliefs and rebates may be shared between qualifying individual taxpayers in mutually agreed proportions; (b) certain personal reliefs may only be applied once on each subject of claim; and (c) certain personal reliefs may be available for claim even though the relevant subject of claim is also the subject of claim of other personal reliefs. The following paragraphs illustrate the above-mentioned features using the Tan family as a case study.

Let us assume that Grandfather suffered a stroke and was paralysed. In addition, he was unable to work and did not derive any income. In this scenario, Grandmother may claim handicapped spouse relief on Grandfather, her husband. Father and Auntie may claim handicapped parent relief on Grandfather, their father. Mother and Uncle may also claim handicapped parent relief on Grandfather, their father-in-law. Similarly, Freeman and Cousin may also claim handicapped parent relief on Grandfather, their grandparent. If all conditions for the above-mentioned personal reliefs were met, who should claim personal relief on Grandfather?

In your analysis, you have to keep in mind that: (a) once handicapped spouse relief is claimed on Grandfather, handicapped parent relief would not be available for claim; and (b) handicapped parent relief may be shared between Father, Mother, Uncle, Auntie, Cousin and Freeman in mutually agreed proportions. Since the quantum of claim for handicapped parent relief could be up to $14,000, which is more than double that of handicapped spouse relief, it should be claimed. The taxpayer(s) with the highest effective tax rate should claim (more of) this relief to achieve optimal tax savings, subject to the personal relief cap of $80,000 effective from YA 2018.

In another scenario, let us assume Freeman and Cousin were both primary school kids, and they were taken care of by Grandmother. In this scenario, Mother and Auntie may claim grandparent caregiver relief on Grandmother, their children’s caregiver. This is notwithstanding that spouse relief and parent relief may also be claimed on Grandmother. If all conditions for grandparent caregiver relief were met, who should claim it? In your analysis, you have to keep in mind that grandparent caregiver relief may not be claimed by Mother, if Auntie has claimed it in the same YA, and vice versa. Hence, if Mother was an administrative assistant and Auntie was an audit partner, the choice would be obvious: Auntie (with a higher effective tax rate) should make the claim.

Consider this: if financial information is not adequately communicated within the family, how would the Tan family be able to conduct tax planning, and minimise personal taxes, effectively and legitimately? Although the communication of financial information with family members is uncommon in the Asian context due to various cultural, social and practical reasons, it could be argued that this communication is necessary for the prevention of wrongful claims in personal tax filings, and the facilitation of effective and legitimate tax planning.

So, gather your family members, start the conversation, and do your maths, before the filing deadline in April.

To conclude, let me echo IRAS in saying, “Thank you for your contribution to nation building!”

Benny E. Chwee, FCA (Singapore) and ATA (Income Tax), is Deputy Head (Master of Management Programme) and Senior Lecturer in Tax Accounting and Law, Singapore University of Social Sciences.