TAKEAWAYS

Over the past four years, I have been interviewing candidates for admission to the Accountancy Programme at the Singapore University of Social Sciences. In the course of doing so, I cannot help but notice a trend – increasingly, candidates are seeking accountancy training to advance their entrepreneurial pursuits. When probed further, candidates believed that doing business is synonymous with incorporating a company. This article explains why incorporating a company may not always work, especially when one is starting small and testing the market.

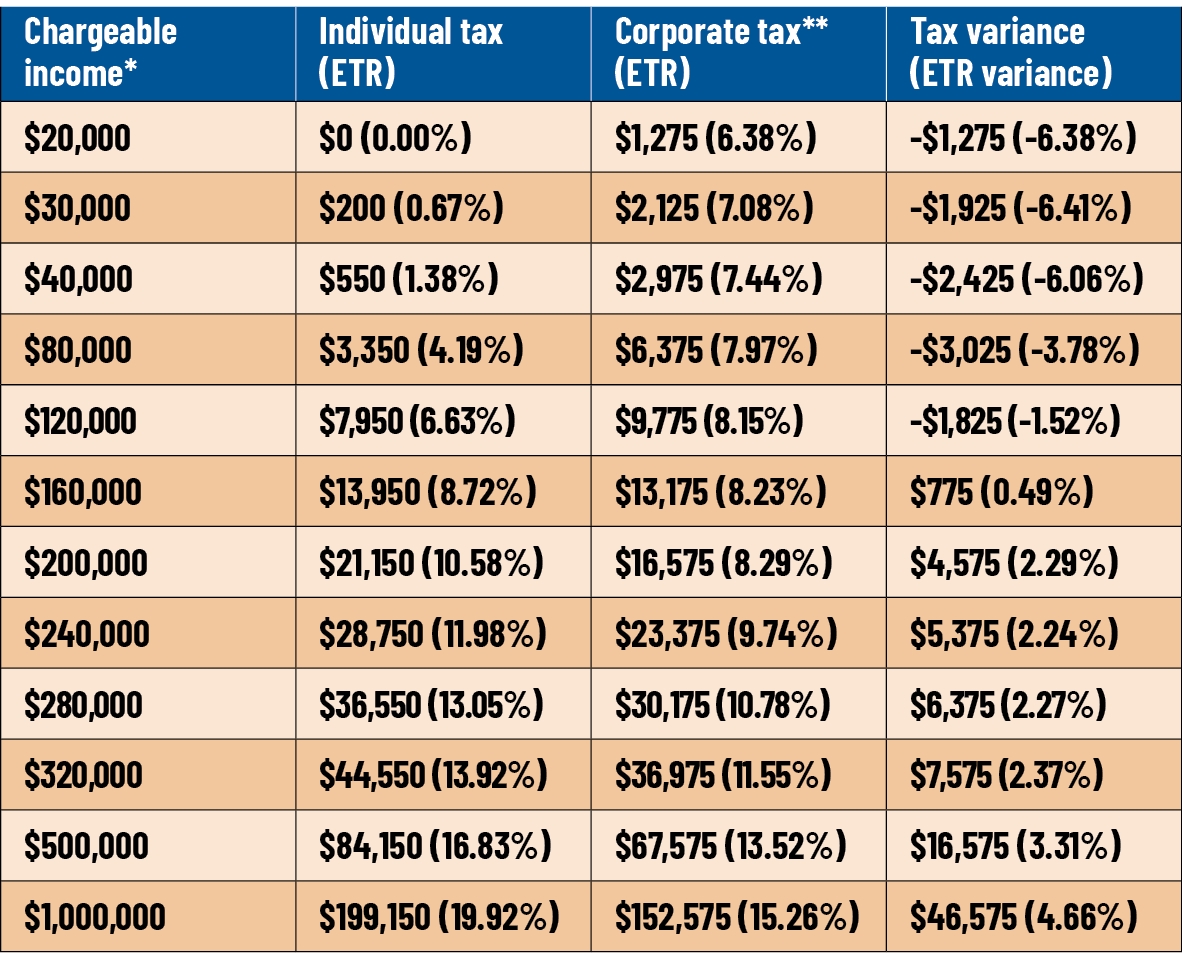

Unlike companies that are subject to income tax at 17%, (tax-resident) individuals are subject to income tax at between 0% and 24%. As a result, an individual who derives chargeable income of no more than $148,077 will generally pay a lower amount of income tax in Singapore vis-à-vis a company. Hence, aspiring entrepreneurs should only consider incorporating a company when their chargeable income is expected to exceed $148,077. Please see the table below for an illustration of effective tax rates (ETRs) at various levels of chargeable income.

Business owners would typically be required to contribute capital for the running of the business. For business structures such as sole proprietorships, general partnerships, limited partnerships and limited liability partnerships, capital may be withdrawn without many restrictions, so long as owner(s) of the business agree. However, the same cannot be said for companies. To protect public interests, the withdrawal of capital may only be achieved through, for example, capital reduction, share buyback and winding up, which are highly regulated and administratively cumbersome.

In addition to the above, business owners would generally be expecting returns on investment. For business structures such as sole proprietorships, general partnerships, limited partnerships and limited liability partnerships, profits may be distributed without many restrictions, so long as owner(s) of the business agree. Again, the same cannot be said for companies. To protect public interests, the distribution of profits may only be made out of after-tax profits with the relevant declaration and approval under the Companies Act 1967.

Incorporating a company is not without costs. At the very minimum, a director and a corporate secretary are required to be appointed. In addition, legal documents, such as a shareholders’ agreement and a constitution (formerly known as the Memorandum and Articles of Association), may have to be prepared, among other documents. Maintaining a company is also not without costs. Statutory registers (and a registered address) have to be maintained, general meetings have to be held, returns have to be filed, etc.

As seen above, incorporating a company in Singapore could be burdensome and expensive. Overcomplicating your business structure prematurely, before the validation of business ideas and achievement of sustainable revenue, may lead to wasted time, effort and money. At the end of the day, the benefits of incorporating a company, such as separate legal personality, perpetual succession and limited liability, among others, must be carefully weighed against the costs of establishing, maintaining and dissolving a company.

Aspiring entrepreneurs ought to be mindful that the benefits of incorporating a company may also be available through other business structures. For instance, a limited liability partnership offers separate legal personality and perpetual succession as a hybrid business structure, combining characteristics of both an incorporated and an unincorporated business structure. Separately, a limited partnership and a limited liability partnership (may) offer limited liability. However, this would be at the expense of management rights in the case of a limited partnership.

As the title of this article suggests, think twice before incorporating a company. There is more than one way to do business in Singapore. Apart from incorporating a company, various business structures, such as a sole proprietorship, a general partnership, a limited partnership and a limited liability partnership, may be established. These structures may provide for efficiency on the tax front, flexibility on the cash front, and effectiveness on the administrative and cost front.

Remember, the law does not meddle with how you do your business – choose your structure wisely.

Benny E. Chwee, FCA (Singapore) and ATA (Income Tax), is Deputy Head (Master of Management Programme) and Senior Lecturer in Tax Accounting and Law, Singapore University of Social Sciences