At the start of the year, the growth for 2025 was predicted to be stable but underwhelming, as reported in the World Economic Outlook (WEO), January 2025 by the International Monetary Fund (IMF). Four months on, however, this forecast no longer holds true as the world has undergone a major shift, when the United States (US) fired a salvo of trade tariffs alongside other policy changes. In the revised figures announced in April 2025, institutions like IMF and the ASEAN+3 Macroeconomic Research Office (AMRO) point to the increasingly volatile and unpredictable global environment as governments relook their policy priorities.

Singapore, as an open economy, is not spared the impact of the rapidly changing external environment. To help members, ISCA shared the perspectives of industry experts and ISCA members, along with potential mitigation measures to the changing circumstances, in a recent CA Lab article.

Revised forecasts

The recent assessments, shared by IMF and AMRO in April, show a moderation of growth in Asia in 2025 and 2026 as a result of the escalating trade tensions and geopolitical uncertainties. The scale-back of international cooperation would also jeopardise progress towards a more resilient global economy. But, given the fluidity of the situation, it is not possible to provide definitive forecast numbers.

IMF’s April update projects global growth to drop to 2.8% in 2025 and 3.0% in 2026 – down from 3.3% for both years (WEO, January 2025). In the emerging market and developing economies, growth is expected to slow to 3.7% in 2025 and 3.9% in 2026, with significant downgrades for countries most affected by the recent trade measures, for example, China, India, and some ASEAN countries.

China’s growth forecast has been lowered to around 4.0% for both 2025 and 2026. India is projected to experience a moderate slowdown to 6.2% in 2025, and 6.3% in 2026. The ASEAN-5 bloc (Indonesia, Malaysia, the Philippines, Singapore, and Thailand) is collectively expected to grow by a revised 4.0% in 2025 and 3.9% in 2026. Global headline inflation will also change, with notable upward revisions for advanced economies and slight downward revisions for emerging markets and developing economies in 2025.

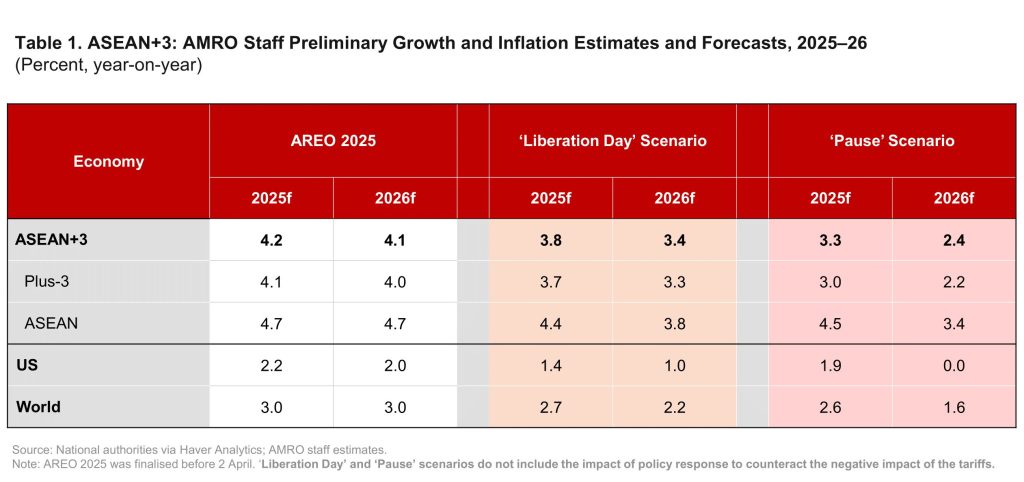

For the region, AMRO, in its ASEAN+3 Regional Economic Outlook 2025 report released in April, says the unprecedented and volatile global trade environment makes it challenging to project specific figures. Instead, its forecasts are given under three possible “scenarios” (Table 1) for the different regions (“+3” refers to China, Japan and South Korea). Similar to IMF, AMRO has lowered the growth forecasts for 2025 and 2026.

What’s next?

Despite the slight variations in their specific growth projections, IMF and AMRO underscore the significant challenges posed by the rising trade protectionism and associated policy uncertainties to Asia’s growth prospects in the near to medium term.

But, Asia is not without options in this period of global turbulence.

As AMRO points out, the region is entering the difficult environment from a position of relative strength and resilience. Firstly, the region’s economies are more balanced than before, with domestic demand and intra-regional trade being primary drivers of growth.

Secondly, the region is now supported by a more diversified external demand structure. The share of exports going to the US has fallen steadily from about 24% in 2000 to below 15% currently. Additionally, intra-regional trade now accounts for 45% of total exports, with China becoming the region’s largest final demand market. This helps to stabilise regional supply chains and demand flows.

Thirdly, many regional economies have fiscal and monetary space, which can be used to support growth and manage downside risks as needed. With the extensive experience from past crises, governments are better able to calibrate the requisite policy mix to mitigate trade disruptions while maintaining economic stability in the months ahead.

AMRO highlights that ASEAN+3’s collective resilience is its greatest asset. Having weathered previous external shocks – from the Asian financial crisis to the global financial crisis and, most recently, the COVID-19 pandemic – the region has strengthened its institutional frameworks and deepened cooperation. The existing challenge is another opportunity to further strengthen regional collaboration.

IMF says countries should work constructively to promote a stable and predictable trade environment and to facilitate international cooperation, while addressing policy gaps and structural imbalances at home. This will help secure both internal and external economic stability. To help themselves, governments can also do more to stimulate growth and ease fiscal pressures.