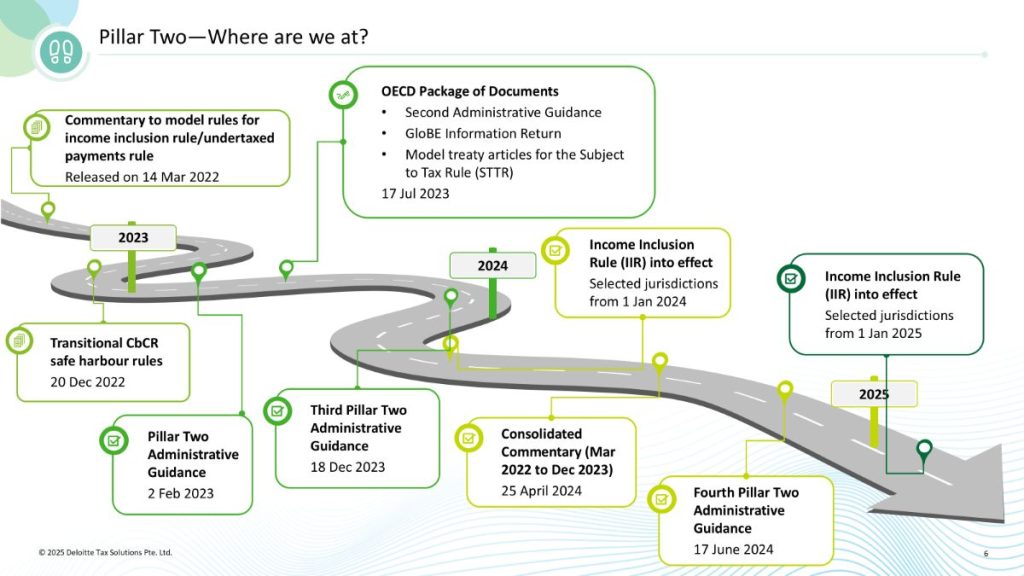

In Budget 2024, Singapore announced that it would implement the Income Inclusion Rule (IIR) and Domestic Top-up Tax (DTT) for businesses’ financial years starting on or after 1 January 2025. This is in relation to the Organisation for Economic Co-operation and Development (OECD)/G20’s Inclusive Framework on Base Erosion and Profit Shifting (BEPS), which aims to ensure that multinational enterprises pay a fair share of tax wherever they operate.

Against this backdrop, on January 15, members attended an ISCA Lunch Talk to find out more about tackling the data and automation challenges posed by OECD’s Pillar Two global minimum tax. The session, held at ISCA House, was helmed by Deloitte Singapore’s International Tax Leader, Liew Li Mei, and Tax Technology Consulting Leader, Piyus Vallabh.

The session offered useful insights into the complexities of managing vast amounts of tax data, and the increasing importance of automation in compliance processes. The discussion focused on how businesses can leverage technology to streamline their tax operations, particularly in addressing the requirements of Pillar Two. The speakers also highlighted the need for robust data collection systems, calculation engines, and analytical tools to efficiently manage complex data flows and accurately determine the effective tax rate for reporting purposes

A key takeaway from the session was the importance of a structured approach in identifying and addressing data gaps. By integrating Pillar Two requirements into existing finance and tax technology systems, organisations can enhance efficiency and manage their compliance risks.