TAKEAWAYS

Singapore does not have a capital gains tax regime. Gains from the sale of all assets that are capital in nature, whether local or foreign sourced, will not be subject to Singapore income tax, whether or not they are accrued or received in Singapore.

Whether a gain from the sale of an asset is treated as capital or revenue in nature is a question of fact. It is determined with regard to the facts or circumstances of each case and with reference to the principles established in case law. The factors considered are drawn from established case law principles, commonly referred to as the “badges of trade”.

However, to address international tax avoidance risks relating to non-taxation of disposal gains in the absence of real economic activities, Singapore has recently amended its foreign-sourced income regime to tax gains from the sale of foreign assets which include:

Where the sale or disposal of foreign assets occurs on or after 1 January 2024, such gains derived therefrom will be taxed when they are received in Singapore under section 10(1)(g) of the Income Tax Act (ITA) if the gains fall within the scope of the new foreign-sourced disposal gains tax regime provided in section 10L of the ITA.

It should be noted that there is no change to the tax treatment of capital gains derived from the sale of local assets which will continue not to be taxable, regardless of when the sale takes place.

The Inland Revenue Authority of Singapore (IRAS) first published an e-Tax Guide (hereafter referred to as the “Guide”) on the tax treatment of gains or losses from the sale of foreign assets on 8 December 2023. It subsequently published the Second Edition of this Guide on 9 December 2024.

The new regime will impose Singapore tax on gains from the sale of foreign assets that were not subject to tax under section 10(1) of the ITA or exempted from tax under the ITA. These gains, termed “foreign-sourced disposal gains”, will be chargeable to tax if the gains are:

In addition, gains from the disposal of foreign IPRs may be subject to tax when they are received in Singapore from outside Singapore by a covered entity, regardless of its level of economic substance.

Section 10L of the ITA will not apply to gains from the sale or disposal of a foreign asset (not being a foreign IPR) when it is carried out:

The foreign-sourced disposal gains are regarded as received in Singapore and chargeable to tax if such gains are:

Foreign entities not incorporated, registered or established in Singapore and not operating in or from Singapore are not within the scope of section 10L of the ITA.

Section 10L of the ITA applies only to entities of relevant groups. An entity refers to any legal person (including a company, limited liability partnership), a general partnership or limited partnership, or a trust.

An entity is a member of a group of entities if its assets, liabilities, income, expenses and cash flows are:

A group is a relevant group if the entities of the group are not all incorporated, registered or established in Singapore, or any entity of the group has a place of business outside Singapore. Therefore, a group with only Singapore entities operating solely in Singapore will not fall within the scope of section 10L of the ITA. However, if any entity in the group has a place of business (for example, a branch or a permanent establishment) in a foreign jurisdiction, the group will be considered as a relevant group for the purpose of section 10L of the ITA.

The economic substance requirement (ESR) is assessed at the entity level and not at the jurisdictional level for a group. Wihere there is a special purpose vehicle (SPV) in a group structure, the holding entity (which can be an intermediate holding entity or the ultimate holding entity) that effectively controls and benefits from the SPV’s activities and defines its core investment strategies, will be the entity subject to the ESR.

The Guide outlines certain criteria for the assessment of economic substance. Generally, these conditions are less stringent for a pure equity-holding entity (PEHE) as compared to a non-pure equity-holding entity (non-PEHE).

A PEHE is an entity:

A non-PEHE is an entity that is not a PEHE.

For a PEHE to meet the ESR, it needs to fulfil all the following conditions in the basis period in which the sale or disposal occurs:

A PEHE will be considered as meeting the ESR if:

A pure registered address (for example, address of the corporate secretary) that is not used by the PEHE’s employees or outsourced service provider to perform the PEHE’s core income-generating activity will not meet the “adequate premises” criterion.

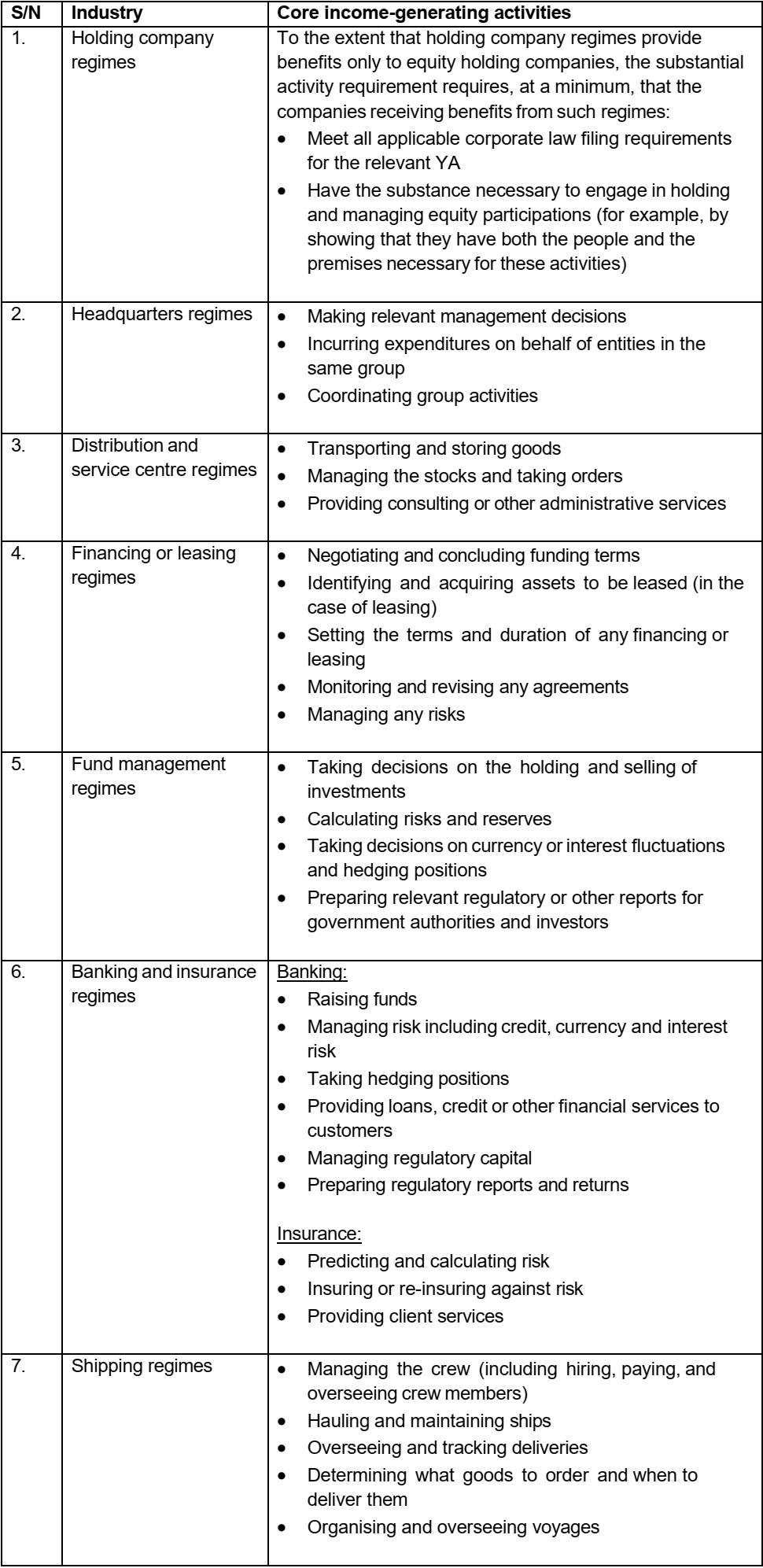

For a non-PEHE, the ESR will be determined based on an analysis of the entity’s core income-generating activities in Singapore. Annex B of the Guide, reproduced as “Annex” at the end of this Part 1, provides guidance on examples of core income-generating activities of some common industry sectors. To meet the ESR, a non-PEHE is required to satisfy all the following conditions in the basis period in which the sale or disposal occurs:

Part 2 of this article continues the discussion, covering how ESR takes into account outsourcing arrangements undertaken by entities; gains from the sale or disposal of IPRs; determining the gains chargeable to tax; tax exemption for individuals, and updates in the Second Edition of the IRAS’ e-Tax Guide.

Simon Poh, FCA (Singapore), is Associate Professor (Practice), Department of Accounting, NUS Business School. The opinions expressed are those of the writer and do not represent the views and opinions of NUS.

Guidance on the Core Income-Generating Activities in relation to the Economic Substance Requirement for Each Sector

The table below covers examples of core income-generating activities of some industries in relation to the economic substance requirement.