TAKEAWAYS

For the past few years, most Pillar Two discussions have focused on understanding the mechanics of OECD’s Global Anti-Base Erosion (GloBE) Rules – effective tax rate (ETR) calculations, top-up tax exposure, and the interaction between the Income Inclusion Rule (IIR), Undertaxed Profits Rule (UTPR) and Qualified Domestic Minimum Top-up Tax (QDMTT).

That conversation is now changing.

As jurisdictions move from policy design to implementation, multinational enterprise (MNE) groups are entering a new phase of the Pillar Two journey: compliance execution.

For Singapore-headquartered groups and foreign MNE groups operating in Singapore, this shift is particularly relevant. While Singapore’s Domestic Top-up Tax (DTT) applies from 1 January 2025, many groups are already facing their first global compliance obligations in respect of FY2024.

For a calendar-year group, the first GIR filing is generally due by 30 June 2026. However, filing GIR is only one part of the compliance picture. Depending on where a group operates, additional obligations such as registrations, local DMTT returns, notifications and tax payments may also apply.

The key question is therefore no longer, “Will Pillar Two impact our tax position?”

It is, increasingly, “Are we operationally ready to comply with Pillar Two across all relevant jurisdictions?”

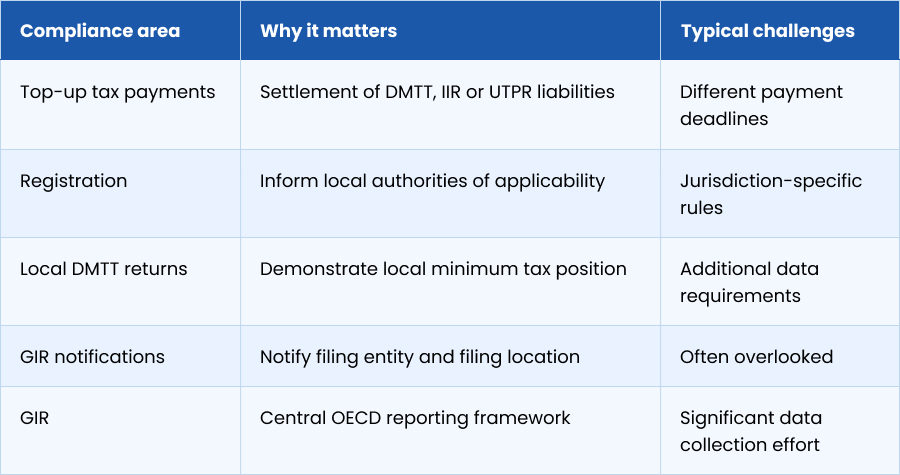

While implementation differs across jurisdictions, Pillar Two compliance generally falls into five broad categories.

GIR remains the cornerstone of the Pillar Two reporting framework. However, many tax authorities have introduced supplementary local requirements, meaning, groups may face multiple compliance obligations arising from the same reporting period.

Unlike traditional corporate tax filings, Pillar Two requires a coordinated global approach. A single reporting cycle may require:

Compounding this challenge is the fact that local implementation continues to evolve. While OECD has provided a common framework, individual jurisdictions have adopted their own administrative procedures, filing forms and deadlines.

As a result, MNE groups need to monitor compliance obligations on a jurisdiction-by-jurisdiction basis rather than relying on a single global filing process.

One of the most common misconceptions is that filing GIR completes the Pillar Two compliance process. In reality, many jurisdictions have introduced additional obligations that operate alongside GIR. These may include:

Table 1: Illustrative Pillar Two compliance requirements across key jurisdictions

The table highlights an important reality: there is no universal compliance model. Even where jurisdictions have adopted the same OECD framework, local administrative requirements may differ significantly.

Many organisations initially viewed Pillar Two as a tax technical exercise. In practice, the biggest challenge often lies elsewhere – data.

The information required for GloBE calculations frequently originates from systems and processes that were never designed for Pillar Two reporting. Common challenges include:

Consequently, successful compliance requires collaboration across multiple functions, including:

For many organisations, establishing governance processes and controls around data collection may prove just as important as understanding the technical rules themselves.

With the first major reporting deadlines approaching, finance leaders may wish to assess readiness across the following five dimensions.

1. Scope assessment

2. Tax exposure assessment

3. Data readiness

4. Global compliance tracking

5. Governance and ownership

1. Treating Pillar Two as a tax department project

Although Pillar Two is fundamentally a tax regime, many of the required inputs originate outside the tax function. Organisations that do not engage finance, legal, treasury and technology teams early often encounter implementation challenges later.

2. Focusing only on GIR reporting

The GIR is only one element of the compliance framework. Local DMTT returns, notifications and registrations can create additional filing obligations that should not be overlooked.

3. Waiting until 2027

As Singapore introduced GloBE Rules in 2025, where the compliance deadline falls in 2027, many groups may not realise that if they have any presence in a jurisdiction which introduced the law in 2024, the compliance deadline falls in 2026. Further, the groups are underestimating the time required to gather, validate and reconcile Pillar Two data. Delaying preparation may increase compliance risk and place unnecessary pressure on finance teams as filing deadlines approach.

The introduction of Pillar Two represents one of the most significant developments in international taxation in recent decades. While understanding the mechanics of GloBE Rules remains important, the immediate challenge for many organisations is operational readiness.

As reporting deadlines for FY2024 approach and Singapore’s DTT regime takes effect, organisations should move beyond high-level impact assessments and focus on compliance preparedness, data governance and cross-functional coordination.

For finance leaders, the question is no longer whether Pillar Two applies. The more important question is whether the organisation is ready for its first global compliance cycle.

Dilpreet Singh, Accredited Tax Advisor, is Tax Partner, Dhruva Advisors.